How do you identify the big cheese at a bank, the decision maker you should sell to? It’s not as easy as it sounds.

Investment banks are notoriously opaque businesses with a characteristic personnel and power structure. Still, there is plenty in common across investment banks and a few generalizations an outsider can make when trying to deal with an investment bank.

The “bulge bracket” are the large investment banks. Bank pecking order and prestige is roughly based on a bank’s size and volume of transactions. Banks who do the most deals generate the highest bonus pool for their employees. The pecking order since the credit crisis is probably:

- Goldman Sachs (NYC)

- JPMorgan Chase (NYC)

- Credit Suisse (Zurich, Switzerland)

- Morgan Stanley (NYC)

- Barclays Capital (London)

- UBS (Zurich, Switzerland)

- Deutsche Bank (Frankfurt, Germany)

- Bank of America / Merrill Lynch (Charlotte, NC)

- Citibank (NYC)

This list is obviously contentious — though Goldman Sachs and JPMorgan are the undisputed masters, and Citibank and BofA are both the train wrecks. BofA is also known as Bank of Amerillwide, given its acquisitions. Bear Stearns opted out of the 1998 LTCM bailout, which is probably why they were allowed to fail during the credit crisis. Lehman Brothers had a reputation for being very aggressive but not too bright, while Merrill Lynch was always playing catchup. NYC is the capital of investment banking, but London and Hong Kong trump in certain areas. I’ve indicated where each of the bulge brackets are culturally headquartered. Each bank has offices everywhere but big decision-makers migrate to the cultural headquarters.

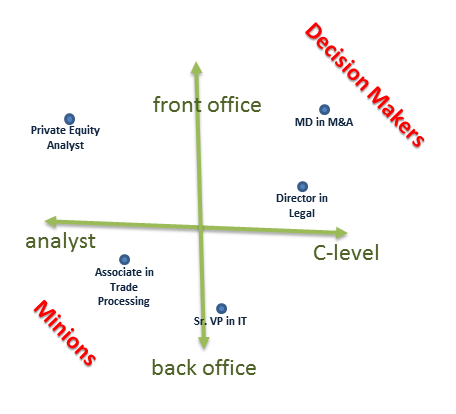

There are two broad axes within each bank. One axis is “front office -ness” and the other axis is “title” or rank. The front office directly makes serious money. The extreme are those doing traditional investment banking services like IPO’s, M&A, and Private Equity. And of course, traders and (trading) sales are also in the front office. Next down that axis are quants and the research(ers) who recommend trades. Then the middle office is risk management, legal and compliance. These are still important functions, but have way less pull than the front office. The back office is operations like trade processing & accounting, as well as technology.

This first front office -ness axis is confusing because people doing every type of work turn up in all groups. JPMorgan employs 240 thousand people so there are bound to be gray areas. An M&A analyst might report into risk management, which is less prestigious than if the same person with the same title reported into a front office group.

The other axis is title or rank. This is simpler, but something that tends to trip up outsiders. Here is the pecking order:

- C-level (CEO, CFO, CTO, General Counsel. Some banks confusingly have a number of CTOs, which makes that title more like:)

- Managing Director (“MD”, partner level at Goldman Sachs, huge budgetary power, the highest rank we mere mortals ever dealt with)

- Executive Director or (just) Director (confusingly lower in rank than an MD, still lots of budgetary power)

- Senior Vice-President (typical boss level, mid-level management, usually budgetary power, confusingly lower in rank than a Director)

- Vice-President (high non-manager level, rarely has budget)

- Assistant Vice-President or Junior Vice-President (“AVP”, rookie with perks, no budget)

- Associate or Junior Associate (rookie, no budget)

- Analyst (right out of school, no budget, a “spreadsheet monkey”)

- Non-officers (bank tellers, some system administration, building maintenance)

Almost everyone at an investment bank has a title. Reporting directly to someone several steps up in title is more prestigious. Contractors and consultants are not titled, but you should assume they are one step below their boss. If someone emphasizes their job function instead of title (“I’m a software developer at Goldman Sachs”), you should assume they are VP or lower. Large hedge funds and asset managers mimic this structure. So to review, who is probably a more powerful decision maker?

- A. an MD in IT at BofA, based out of Los Angeles -or- B. an ED in Trading also at BofA, but based in Charlotte (highlight for the answer: B because front office wins)

- A. an MD in Risk Management at Morgan Stanley in NYC -or- B. a SVP in M&A also at Morgan Stanley in NYC (A because title wins)

- A. a Research Analyst at JPMorgan in NYC -or- B. a Junior Vice-President in Research at Citibank in London (A because NYC and front office wins)

- A. a VP Trader at Morgan Stanley in Chicago -or- B. an SVP in Risk Management at UBS in London (toss up, probably A since traders win)

- A. an Analyst IPO book runner at Goldman Sachs in NYC -or- B. an Analyst on the trading desk at JPMorgan in NYC (toss up, probably A because Goldman Sachs wins)