Ever wondered why your flat’s Zestimate bounces around so much?

In high school economics class you might have learned about fungible goods. This strange word refers to things that could be swapped without the owners especially caring. A dollar is almost perfectly fungible, and so is an ounce of pure silver. Paintings and emotional knick knacks are not at all fungible. Fungible stuff is easy to trade on a centralized market, since a buyer should be happy to deal with any seller. This network effect is so important that markets “push back,” and invent protocols to force fungibility. Two arbitrary flatbeds of lumber at Home Depot are probably not worth the same amount of cash. However the CME’s random length lumber contract puts strict guidelines on how that lumber could be delivered to satisfy the obligation of the future contract’s short trader.

Real estate is seriously non-fungible. Even a sterile McMansion in the suburbs can have a leaky roof, quirky kitchen improvements, or emotional value for the house-hunting recent college grads. If we consider many similar homes as a basket, or a portfolio of the loans secured by the homes, then the idiosyncrasies of each home should net out to zero overall. Across those ten thousand McMansions, there should be a few people willing to pay extra for a man cave, but also a few people who would dock the price. This is the foundation of real estate “structured products,” such as the residential mortgage backed securities (RMBS) of recent infamy. Like flatbed trucks delivering a certain sort of wood for a lumber futures contract, a RMBS makes a non-fungible good more fungible.

The Usual Place

The combined idiosyncrasies of non-fungible things rarely net out to exactly zero, especially during a financial crisis. Nonetheless traders and real estate professionals want to think about a hypothetical, “typical” property. We define a local real estate market by city, neighborhood or even zipcode. How do we decide the value of a typical property? There is an entire industry built around answering this question. One simple, clean approach is to sample a bunch of real estate prices in a local market at a certain point in time, and then average the prices. Or maybe use a more robust descriptive statistic like the median price.

The most readily available residential home prices in the U.S. market are “closed” transactions, the price a home buyer actually paid for their new place. Using a closed transaction price is tricky, because it is published several months after a property is sold. Can a typical home price really be representative if it is so stale?

Sampling

Even if we ignore the time lag problem, there is another serious challenge in using transactions to calculate a typical home price. Within any local real estate market worth thinking about, there are very few actual transactions compared with overall listing activity and buzz. Your town may have a hundred single-family-homes listed for sale last week, but only four or five closed purchases. A surprise during the buyer’s final walkthrough could wildly swing the average, “typical” home price. For the statistically inclined, this is a classic sample size problem.

There are plenty of ways to address the sample size problem, such as rolling averages and dropping outliers. Or you could just include transactions from a wider area like the county or state. However the wider the net you cast, the less “typical” the price!

Another approach is to sample from the active real estate market, those properties currently listed for sale. You get an order of magnitude more data and the sample size problem goes away. However everyone knows that listing prices do not have a clear cut relationship with closing price. Some sellers are unrealistic and ask too much, and some ask for too little to start a bidding war. What is the premium or discount between listing price and actual value? We spend a lot of time thinking about this question. Even closed transaction prices are not necessarily the perfect measure of typical “value” since taxes and mortgage specifics can distort the final price. Our solution is to assume that proportional changes in listing prices over time will roughly match proportional changes in the value of a typical house, especially given a larger sample from the active market.

A Picture

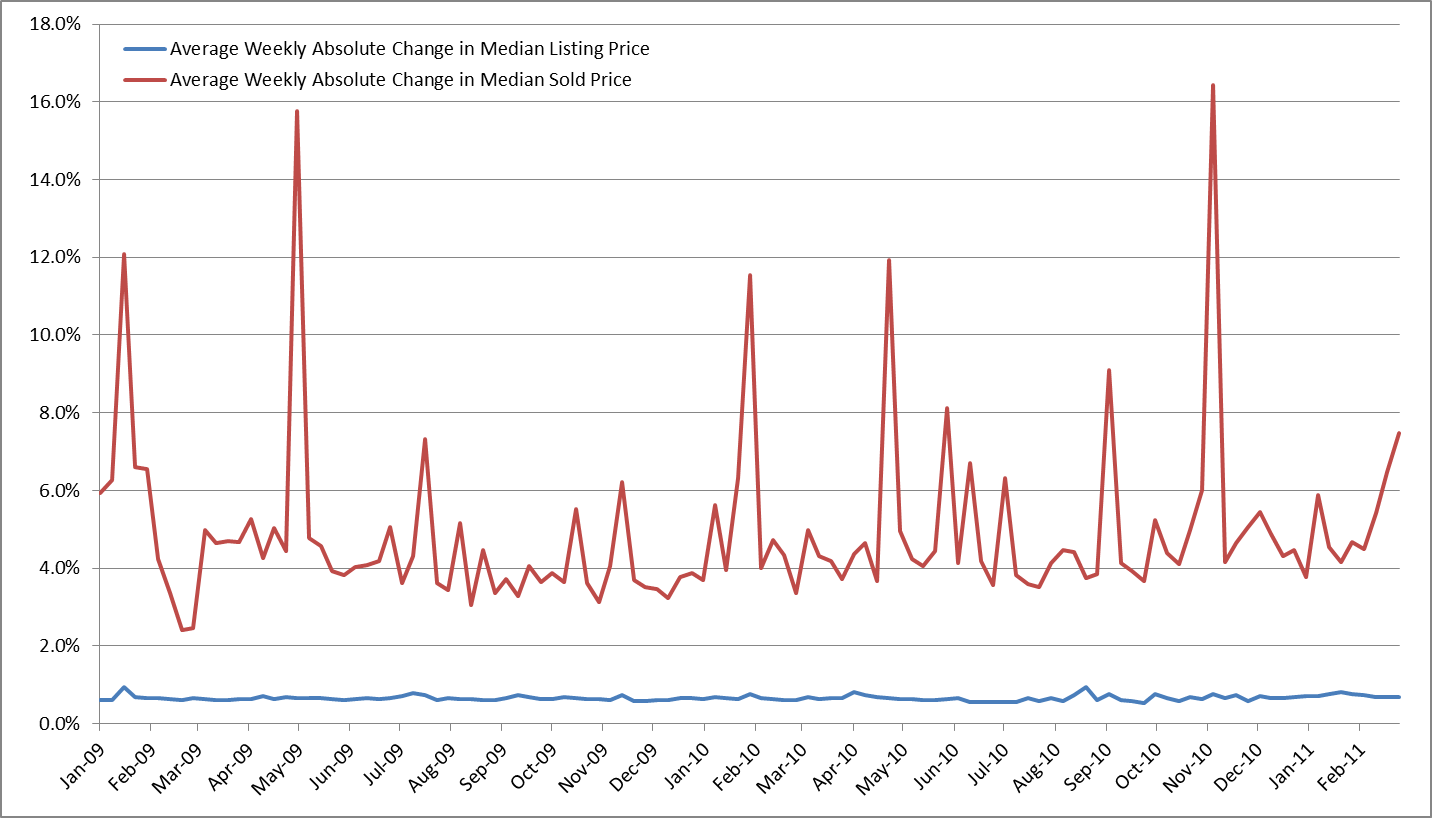

Below is a chart of Altos Research‘s real estate prices back through 2009, across about 730 zipcodes. For each week on the horizontal axis, and for each zipcode, I calculate the proportional change in listing price (blue) and in sold price (red) since the previous week. Then I average the absolute value of these proportional changes, for a rough estimate of volatility. The volatility of sold prices is extreme.